The cost of raising children has increased significantly over recent years with an average high income family’s estimated spending for two children being almost $1.1m from birth until they finish their education. The largest single contributor to these costs was the cost of education, at around 21% of total child raising costs.ᵃ Both primary and secondary education costs increased enormously, with preschool and primary education almost doubling in cost, and secondary education more than doubling in cost over the previous five years.

We all know the rising cost of education is expected to continue. According to the Australian Bureau of Statistics’ Household Expenditure Survey, it found that education costs rose by 44% in the six years to 2016.ᵇ

Recent studies have shown that 45% of Australian families will educate their children in the private school system. Throw in incidentals like excursions, books, laptops and uniforms and there’s no doubt about it – giving a child a good education can be expensive.

How do you make sure you have the choice of education options when the time comes? The key is to have a plan, start early and consider an investment bond for a tax effective, flexible investment solution. While it may seem crazy to start planning for a child’s education in their infant years, investing in an education is a long-term investment that needs a long-term savings plan. By starting early you’ll have more money available when you need it.

How an investment bond can help

Investment bonds are a tax effective way to save for the cost of education as they are a tax paid investment. This means the tax paid on investment earnings is paid by us (Generation Life) at a tax rate up to 30%. Investors don’t need to declare any annual income from their bond in their annual tax returns.

Benefits of a regular savings plan

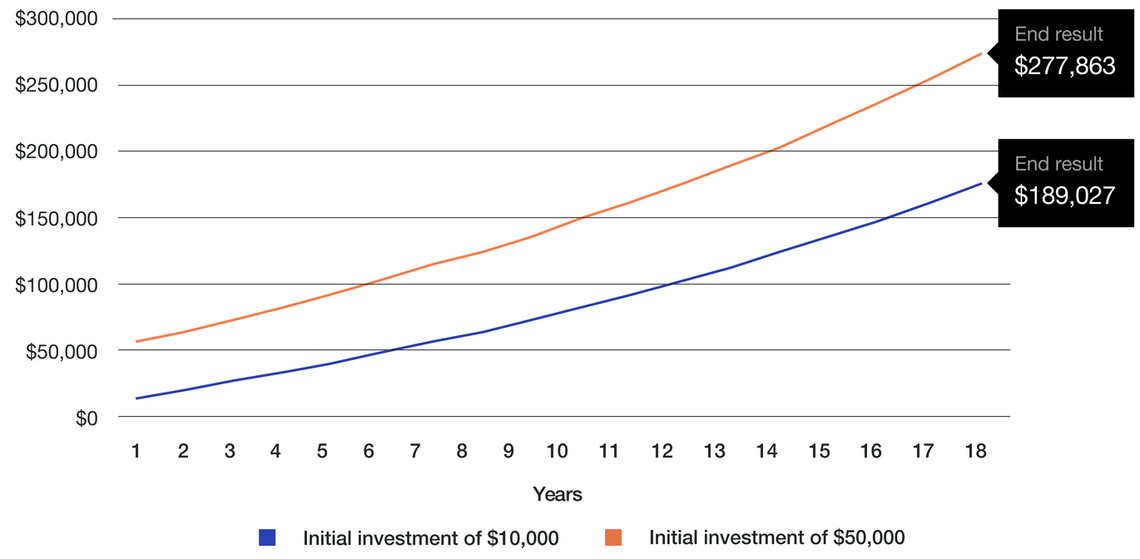

Investment bonds are flexible investments and you can choose to make regular contributions from as little as $100 per month. Setting up a direct debit is a way to grow your investment without even having to think about it. Add compound interest into the mix and you’ll be packing them off to the best school before you know it.

Your friend: compound interest

Described by Albert Einstein as 'the most powerful force in the universe', compound interest is worth understanding if you’re serious about growing your wealth. Simply put, compound interest means that you receive interest not only on your initial investment but also on the prior interest added to your investment. Meaning that your total return grows exponentially the longer the time frame. The longer you can keep your investment untouched the more your wealth will grow.

Here’s how: