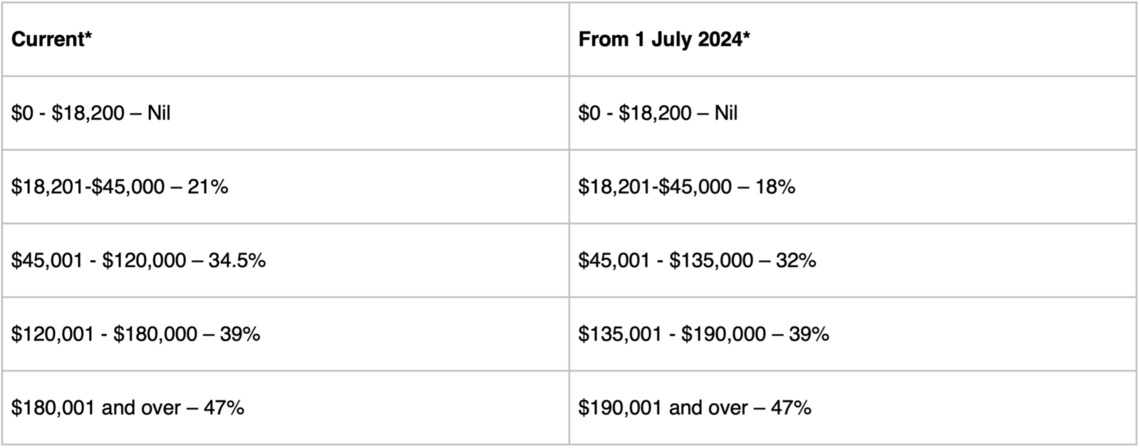

Stage 3 tax cuts offer the opportunity for tax-efficient strategies

Amidst these changes, investors have a unique opportunity to explore investment structures that can be tax efficient, to mitigate the impact of bracket creep. Superannuation remains a highly tax-effective way preserve savings to provide for retirement, offering concessional tax treatment of contributions and favourable tax rates on earnings within the fund. However, it's essential to note the evolving regulatory landscape, such as the proposed Division 296 tax on large superannuation balances², requiring careful consideration in financial planning strategies.

For those seeking alternative or additional avenues for tax optimisation to accumulate wealth, investment bonds emerge as a compelling solution. Operating as a tax-paid structure, investment earnings from an investment bond do not form part of your personal taxable income and can help avoid the potential of creeping into the next tax bracket and unexpected tax liabilities. Any income you receive from an investment bond doesn’t contribute to your overall taxable income, helping you to reduce the overall impact of bracket creep.³

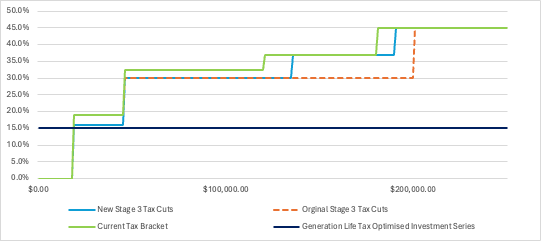

Embracing the benefits of investment bonds

As a leading innovator in the tax-aware investment space, Generation Life has pioneered a forward-thinking approach to providing higher after-tax returns through our new generation of investment bonds. Our focus on minimising the impact of tax on returns, particularly for investors above the 30 percent marginal tax rate, sets a new standard in tax-efficient investing that complements superannuation. Our market-leading tax-aware approach and in particular, our growth-orientated investment options are estimated to further reduce the investment bond’s long-term effective tax rate to just 12-15 percent⁴, with no additional investment risk.

Chart 2: Generation Life’s Tax Optimised Investment Series long-term effective tax rates regardless of an investor’s tax bracket