Managing the retirement risk of longevity, or in other words, outliving their savings and suffering a reduction in retirement lifestyle is one of the key challenges facing Australian retirees. Another common challenge is where people run the risk of experiencing regret in the later years of retirement because they live too frugally in the early years of retirement with an unnecessarily constrained retirement lifestyle. So how can you ensure you live an enjoyable and fulfilling retirement and avoid regret risk?

Why lifetime annuities

A lifetime annuity should form a big part of the discussion with your financial adviser, when working on a retirement income strategy. “The lifetime annuity puzzle is just that - if you’re trying to fund your retirement, the lifetime annuity is a very efficient way to do that.” Wade Pfau, author of Safety First Retirement Planning. A lifetime annuity provides a disciplined structure that helps retirees optimise returns, lock-in income and manage longevity. The opportunity of regular income payments over the course of your retirement could be the missing link when it comes to upgrading their retirement lifestyle and combating regret risk in the later years of retirement.

Higher returns & higher incomes with an investment linked lifetime annuity

The Australian lifetime annuity market has traditionally been dominated by fixed income annuities and a long lasting, low rate environment has reduced the attractiveness of these products. Recently innovation in the lifetime annuity market has seen the introduction of a new type of lifetime annuity. Investment Linked lifetime annuities offer the potential for higher overall returns and therefore higher income payments during the life of the lifetime annuity.

Financial advisers can help find your optimal mix for retirement - balancing income, access to savings, lifestyle objectives, risk, social security and estate planning considerations. When considering your ideal retirement strategy, we recommend consulting a financial adviser to make sure your current and future investments are structured to meet your retirement objectives.

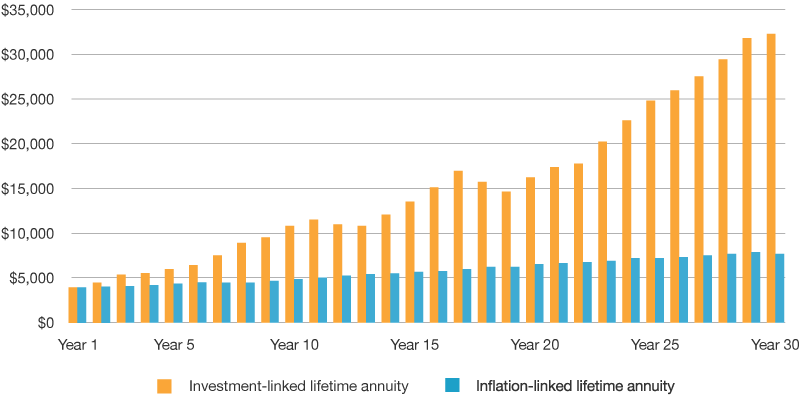

Investment-linked vs. inflation-linked lifetime annuity

The graph below illustrates how an investment-linked lifetime annuity has the potential for annual income to grow over time when compared to an inflation-linked lifetime annuity.