Introducing LifeIncome LifeBooster

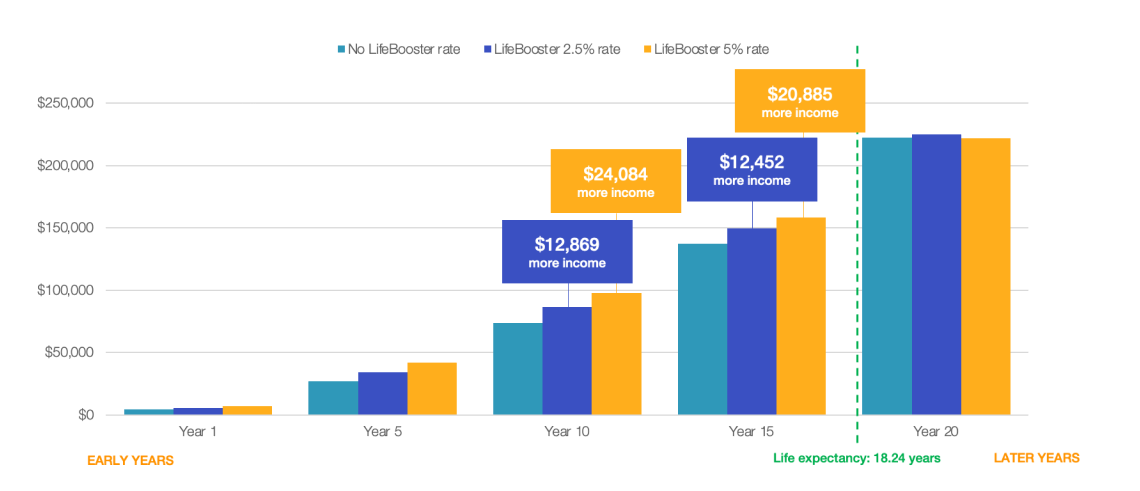

Research in Australia and globally shows that spending in retirement actually declines over time. Spending tends to slow at around 70 and decreases rapidly after 80. What if you could actually bring retirement income forward into the earlier years of retirement? Generation Life has developed a feature within its new and innovative investment-linked lifetime annuity that does just that.

Generation Life’s new lifetime annuity - LifeIncome - is designed to optimise your retirement income and complement other retirement solutions such as an account-based pension. A key feature of LifeIncome is LifeBooster which enables you to receive more income in the earlier years of retirement.

LifeIncome offers you the choice of two LifeBooster rates that enables you to optimise your starting income while aligning to your longer term retirement goals and objectives.

The power of LifeBooster

Access to more income sooner

To enable you to tailor your income requirements over time, LifeIncome offers two LifeBooster rates of 5% and 2.5%, which optimise starting your income while still allowing your income to grow over the life of your investment.

Optimise your starting income with LifeBooster

-

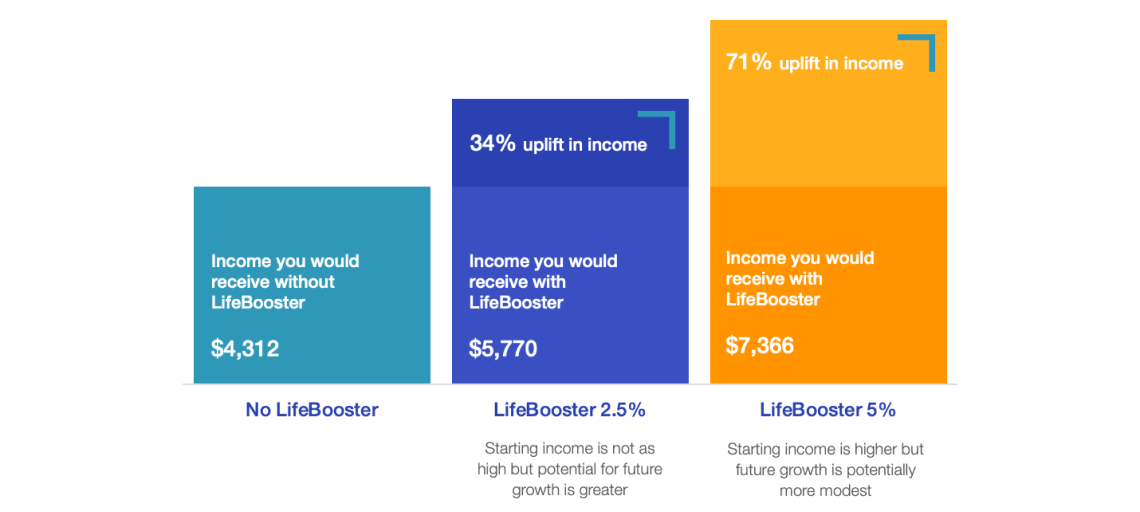

Your starting income can increase by as much as 71% compared to if no LifeBooster rate was applied.*

-

Your investment is paid back in the form of cumulative income sooner.

-

You will receive more income in the early years when you’re more active and able to enjoy it.

To illustrate the benefits, let’s compare how LifeIncome would work with and without LifeBooster.

Comparing first year income