When taxes go down, returns go up. It’s that simple.

At Generation Life, we’re passionate about continuing to innovate to achieve higher returns whilst lowering your personal tax burden. That’s why we’re excited to offer investors our market leading innovations through our Tax Aware Investment Series.

How do we increase performance without taking on additional investment risk?

-

Good turnover of assets and the ability to offset a capital loss against income, unique to the investment bond tax structure.

-

Updated tax management process. We have the ability to choose which parcel of securities to buy or sell, minimising the impact of tax unlike traditional investment practices.

-

Not buying into unrealised and realised gains tax positions. All tax positions are factored into the

unit price.

-

We are able to stay invested for longer and increase the compounding effect generated on your investment.

The after-tax return benefits of an investment bond

Investment bonds are a tax-effective way to accumulate wealth. The returns and performance from an investment bond are provided on an after-tax basis – unlike other investments such as managed funds, shares, property and term deposits where the returns are before the deduction of tax.

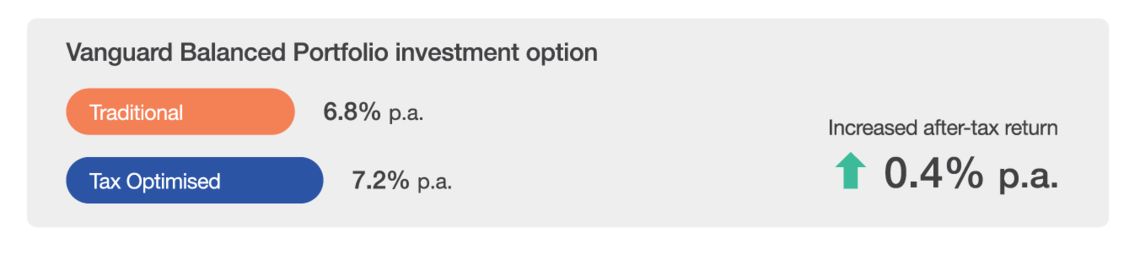

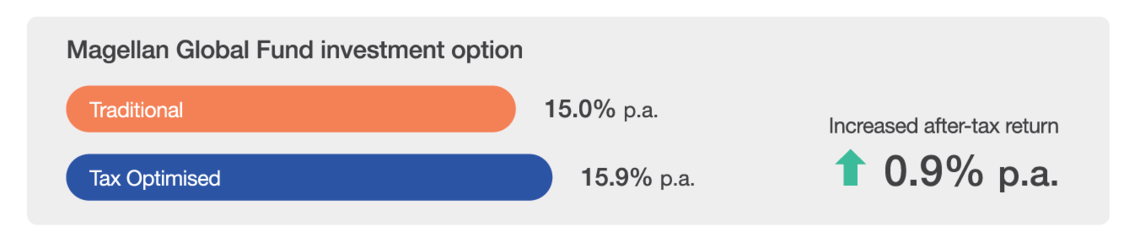

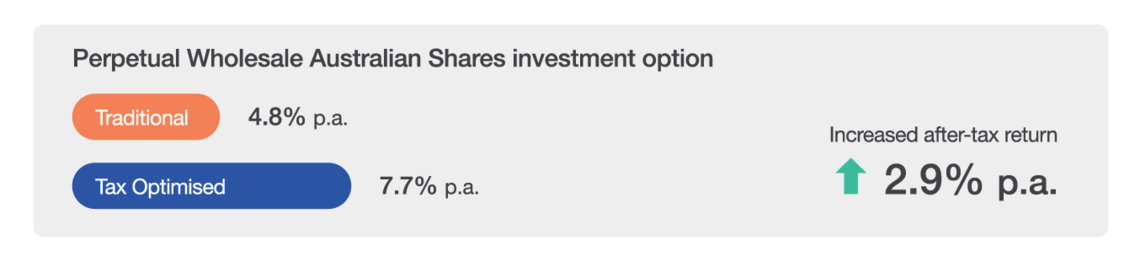

The following examples illustrate the after-tax benefit when applying the Generation Life Tax Optimised structure. This approach has demonstrated an increase in after-tax performance of between 0.4% and 2.9% per annum, over the long term. The best part is, it’s the same investment strategy, with zero additional risk.

Illustrative performance differential - Traditional versus tax optimised investment bond

The following case studies demonstrate the relative improvement in returns for each of the investment options had they been invested based on a traditional approach versus the Tax Optimised approach.

Over the long term, the Tax Optimised approach has demonstrated an increase in returns as a result of its tax aware approach and structure.