Introducing LifeIncome

The most flexible and innovative investment-linked lifetime annuity in the market.

Available exclusively through your financial adviser, LifeIncome is designed to complement other retirement income sources and provide certainty when it comes to meeting your retirement goals.

Below are six core uses of LifeIncome:

- Potentially qualify or bring forward the age to access the Age Pension and ancillary benefits.

- Minimising the impact of an inheritance on your Age Pension benefits and providing regular income guaranteed for life.

- Protecting your spouse / loved one with income for life or a death benefit payment.

- Providing peace of mind and confidence to spend your retirement savings and avoiding ‘regret risk’.

- An additional income layer alongside your account-based pension and Age Pension.

- Investment choice that aligns to your risk profile with the ability to switch at anytime1 as this changes throughout your retirement.

Access more of the Age Pension

LifeIncome is defined as an ‘asset-tested income stream (lifetime)’ product for social security purposes and provides the potential to access some or more of the Age Pension and ancillary benefits such as discounted council rates and cheaper medicine under the Pharmaceutical Benefits Scheme.

Centrelink and the Department of Veterans’ Affairs entitlements are determined using two ‘means’ tests: an assets test and an income test.

Means tested asset value

Under the assets test, only 60% of your investment amount is assessed. From age 84, subject to a minimum of 5 years from the date of investment, only 30% is assessed.

Year 1 means tested income

Only 60% of your LifeIncome annual income is assessed under the income test.

Investment choice and flexibility

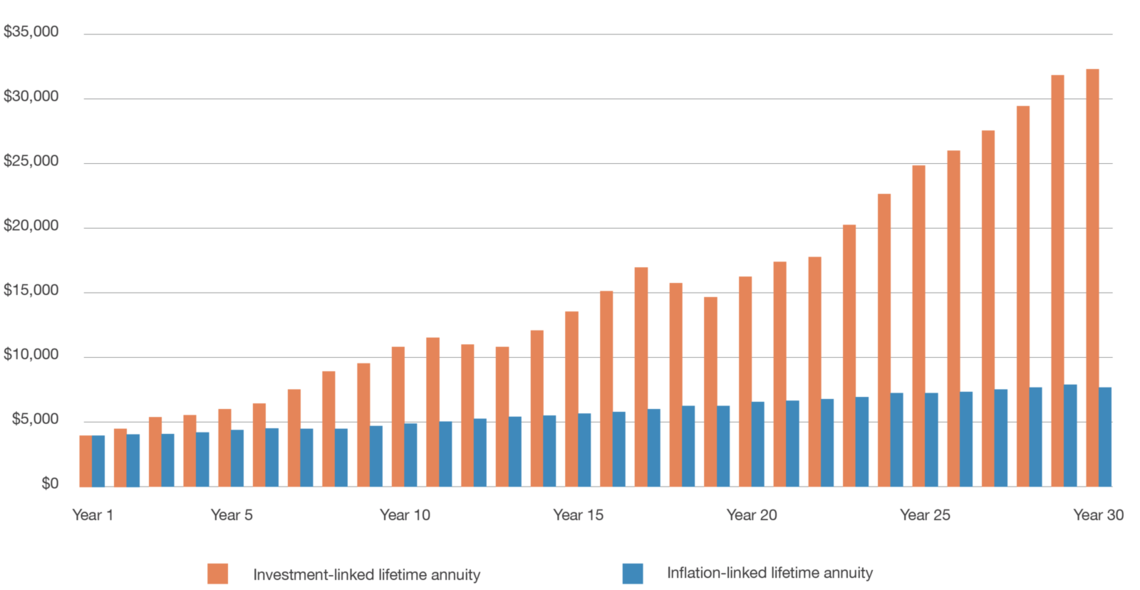

Traditional lifetime annuities have only offered a fixed-rate return or an indexed return (e.g. CPI-linked).

Due to LifeIncome’s investment-linked structure, changes in annual income are linked to the investment performance of your chosen investment option(s). The income payments will go up and down with investment performance, and over the longer term income can be expected to grow in excess of inflation, depending on the investment option(s) chosen.

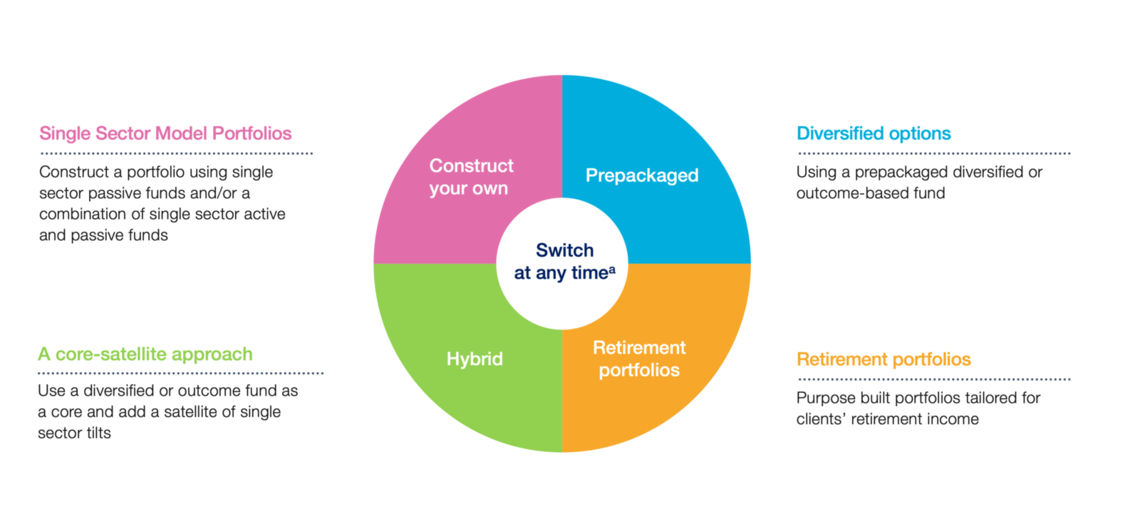

LifeIncome offers a wide range of investment options across all major asset classes including shares, infrastructure and private debt, with the ability for you to switch these investment option(s) at anytime.ᵃ

Working closely with your financial adviser, you can build your own portfolio by investing in single asset investment options or use one of the diversified investment options to suit your desired risk profile. So if your risk profile changes then so too can your investment.

Four portfolio construction ideas