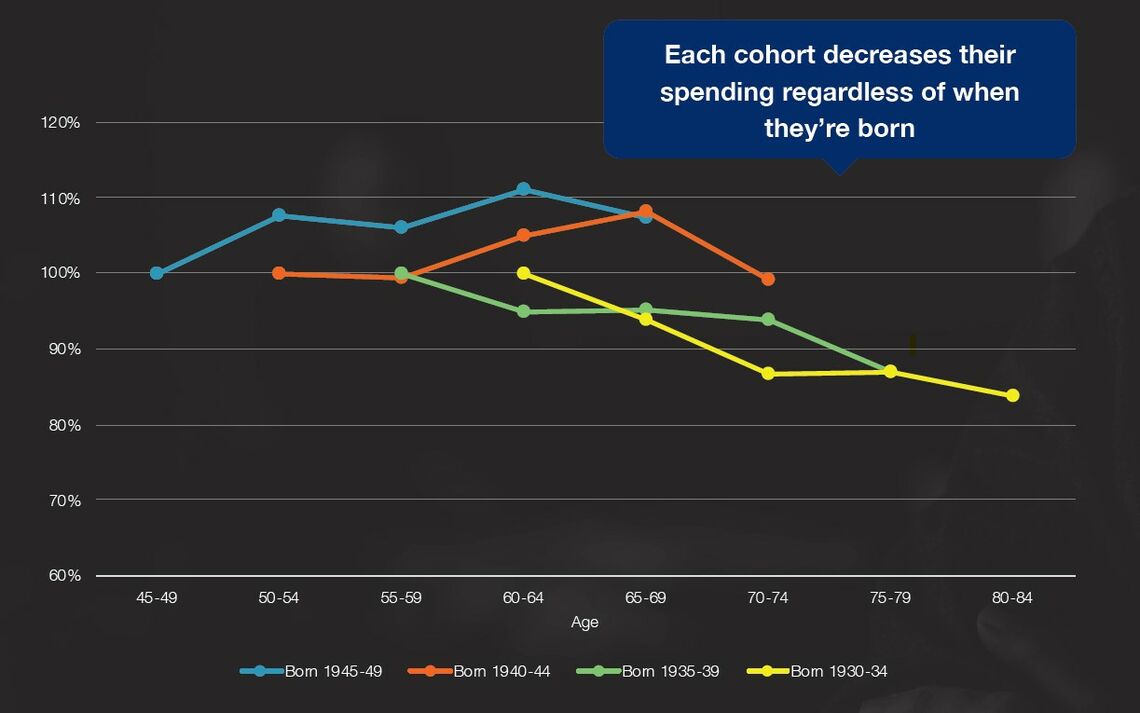

Studies also show that where retirees include a lifetime annuity, like LifeIncome, in their retirement portfolio, they spend more and have the freedom to enjoy their retirement. Conversely, where people haven’t implemented a solution to prevent them from running out of money, those people live more frugally and save their retirement savings, rather than spend them.

Avoid regret risk in the later years of retirement

LifeIncome Flex offers you the opportunity to help you avoid experiencing ‘regret risk’ at the end of retirement, when you look back and wish you hadn’t lived so frugally in those early years, not knowing how long your money was going to last.

At Generation Life, we understand retirement is an emotional journey, not just a financial decision and we want all Australians to have the opportunity to enjoy their retirement. That’s why we’ve introduced LifeIncome Flex, allowing you to increase your income and help you make the most of your retirement. Your retirement is a well deserved reward after years of hard work, not a time to worry about your savings and whether you’ll run out of money.