Division 296, proposed in 2024 was to add a new layer of complexity to an already complicated landscape. With other tax reforms now anticipated following the government’s recent Productivity Roundtable discussions, advisers who rely on “business as usual” to deal with the financial regulatory environment may risk overlooking one of the most tax-effective and flexible structures available: investment bonds.

At the recent Productivity Roundtable discussions, the government reinforced its commitment to reshaping Australia’s tax system to ensure sustainability and equity, with wealth taxes still one of the areas of focus. Over the past decade, there have been constant changes to superannuation - from the introduction of Division 293 in 2012, to the legislated objective of super in 2024, and the government’s lastly proposed Division 296, which would impose an additional tax on earnings from super account balances above $3 million, has yet to be confirmed as abandoned.

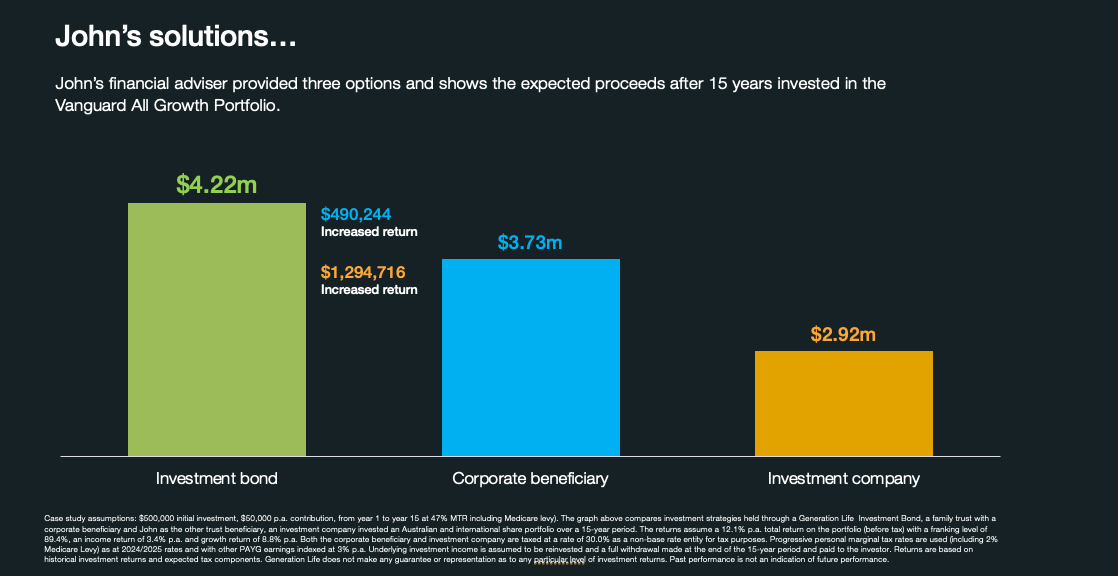

Financial advisers are exploring strategies as tax and regulatory reforms increasingly constrain wealth structures. With clients seeking alternative solutions for wealth accumulation and intergenerational transfers, investment bonds continue to gain strong momentum as one of the most flexible and tax-effective options.

Why investment bonds aren’t as “niche” or “old-fashioned” as you may think.

A prevailing view among advisers is that investment bonds are defined by capped tax and the 10-year rule. But that’s only part of the picture. In reality, investment bonds have evolved into a far more versatile structure - supporting tax-effective, wealth transfers and estate planning peace of mind.

Here are seven features that make them worth a second look:

1. Tax paid, not tax passed on

Unlike trusts that ordinarily push taxable distributions onto clients each year, investment bonds are internally tax-paid (up to 30%) with no distributions. In practice, tax-aware investment options available within some investment bonds can help achieve much lower long-term effective annual tax rates - often in the 10–15% range¹. That means no messy end-of-year surprises such as unplanned assessable income and unforeseen tax consequences, that may enable far greater predictability for long-term planning.

2. More control over wealth transfers

Investment bonds can be structured to sit outside the estate and allow clients to nominate beneficiaries directly - even with conditions. Nominations are binding, providing greater certainty that the death benefit will be paid tax-free to the intended recipient(s). Ownership can also be transferred seamlessly across generations (or to any person for that matter) either while the investment is held, upon the passing of the owner or a future date, all without triggering an assessable tax event.

3. Access without the handcuffs

Clients can withdraw funds from an investment bond at any time if life takes an unexpected turn. Such flexibility and structure make investment bonds a more than viable vehicle to seriously consider.

4. A tool against “bracket creep”

Earnings are taxed and held within the investment bond with otherwise distributable income accumulating. Investment bonds can help shield clients from being pushed into higher brackets, by not distributing assessable income year-on-year. For clients worried about rising personal tax rates, this can help manage and improve after-tax outcomes.

5. Estate certainty and creditor protection

When structured as a non-estate asset, an investment bond may mitigate estate disputes and challenges - ensuring wealth lands exactly where clients intend. That level of comfort is a strong differentiator particularly when the success rate for estate challenges is 74%². Investment bonds appropriately structured can also be protected from creditors in the event of bankruptcy of the owner.

6. The truth about the 10-year rule

Often misunderstood as a lock-up, it’s really a tax-timing benefit. Clients can withdraw anytime - but after 10 years (if the 125% rule is followed), withdrawals are completely non-tax assessable. Importantly, contributions can continue (provided the 125% rule is met) without resetting the clock.

7. Simplicity and freedom from red tape

No TFNs, no annual tax returns, no CGT tracking. Also, there are no contribution caps, withdrawal age limits, or preservation rules. Clients can contribute lump sums or regular amounts, and invest in a wide menu of investment options according to their risk profiles.

How investment bonds may be used

Super, trusts and companies all have their place. The unique features of investment bonds means that, in the right scenarios, they can deliver stronger after-tax outcomes for clients, often with less complexity. The key is knowing when - and how - to integrate them.