Similar to superannuation, investment bonds offer a tax effective solution for building wealth, with tax on investment earnings capped at 30%. In some cases, this can be even lower after franking credits and tax deductions are applied. This tax benefit is particularly attractive to high income earners with a marginal tax rate higher than 30%.

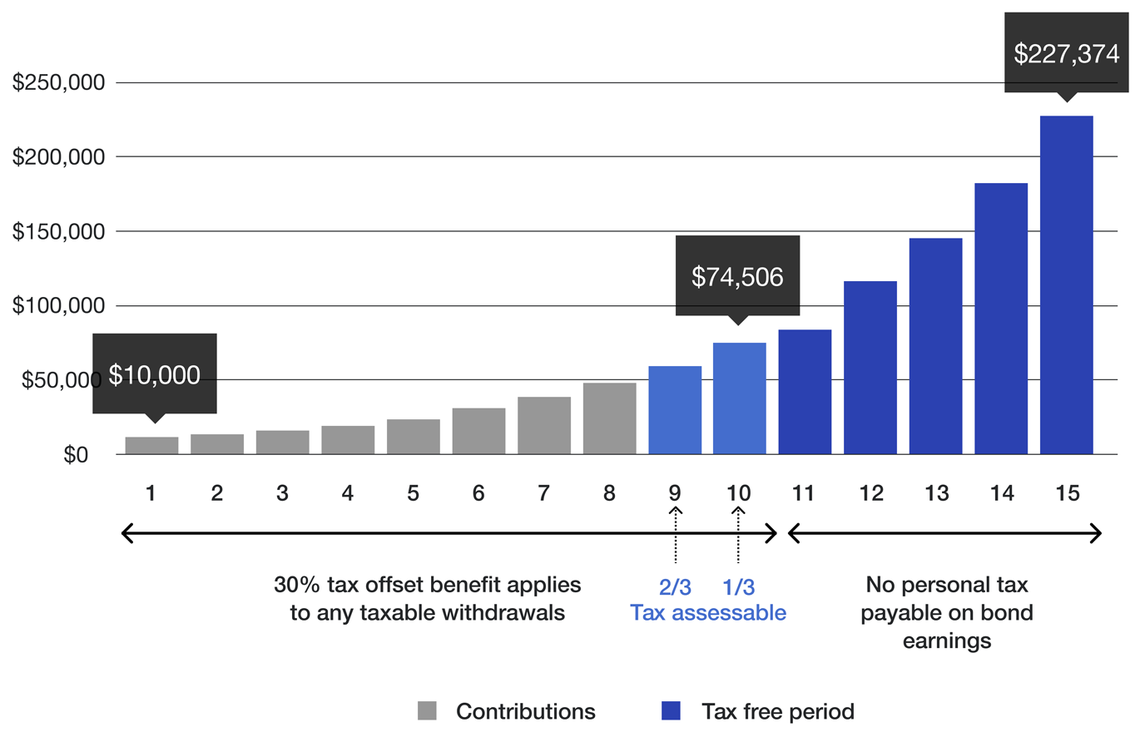

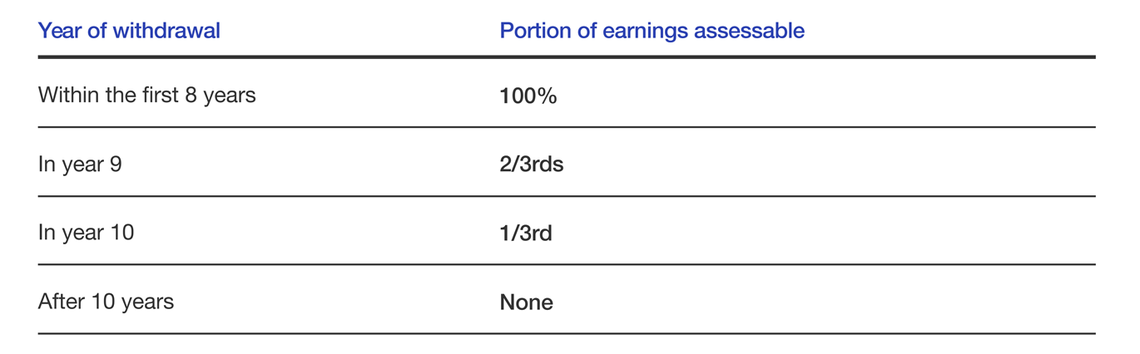

Investment bonds offer other advantages over superannuation, they do not have any restrictions on your initial investment amount, withdrawals prior to preservation age, and there are no limits on subsequent contributions. Another key tax feature of investment bonds is that if the investment is redeemed after 10 years, no personal tax is paid on the proceeds by the investor.

If you’re looking for a tax effective, flexible way to save for retirement outside the superannuation system then investment bonds are worth considering.

Why are investment bonds so tax-effective?

The main appeal of investment bonds is their tax benefits, particularly for those on moderate to higher rates of personal tax and with income surplus to their lifestyle needs. The tax treatment is simple: tax is paid within an investment bond rather than personally by the investor. Plus, when held for 10 years no personal tax is paid by the investor on any future withdrawals.

The 10-year tax advantage

The advantage of holding onto it for at least 10 years is there’s no personal tax payable on withdrawals. The beauty of an investment bond, if we were still to compare against superannuation, is that you can withdraw all, or part, of your investment at any time unlike having to wait until you’re 65.

125% opportunity - tax free after 10 years