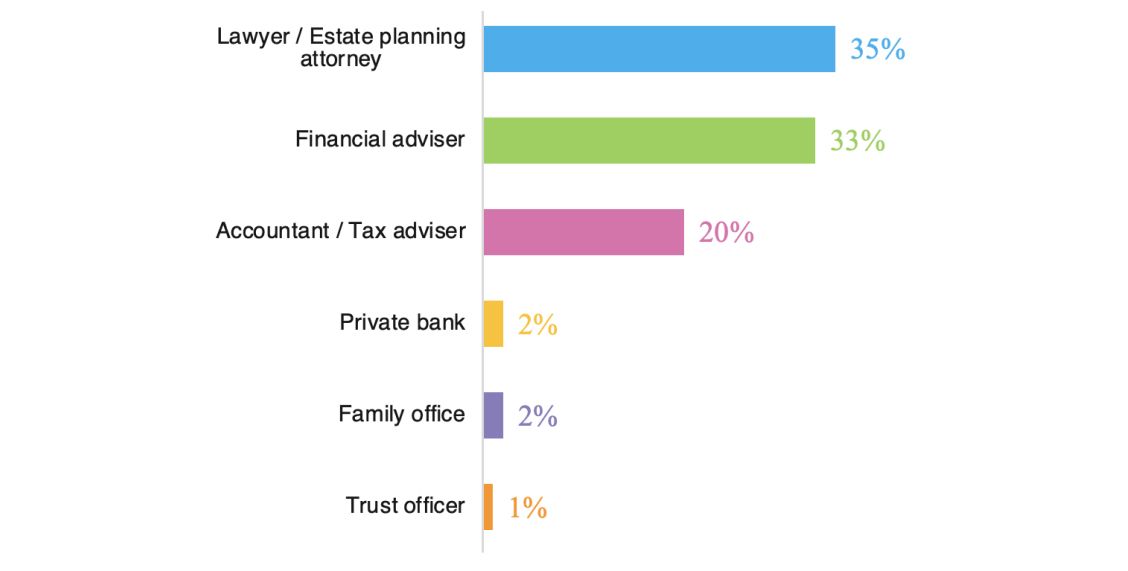

Strategies for mastering estate planning

Estate planning is crucial to ensuring wealth is transferred efficiently while reducing the likelihood of tax implications and potential estate challenges such as disputes from unintended distributions, and inadequate structuring of assets. Without effective planning and having the right structures in place, your clients may not have their wealth transferred in the way they intended, impacting their loved ones and their legacy.

1. Facilitate early inheritances

There’s a growing trend of early inheritances, especially as property prices and the cost of living rises. Many parents prefer to see their loved ones benefit from their wealth during their lifetimes. You should explore whether your clients wish to pass on wealth before their passing and guide them with the best strategies to achieve this.

2. Understand tax implications

You need to ensure your clients understand the tax implications associated with different asset structures, such as superannuation, trusts, and investment bonds. For example, superannuation carries a death benefit tax for non-dependant beneficiaries; investment bonds offer tax-free wealth transfers, regardless of the recipient’s dependency status.

3. Structure assets effectively

Holding assets in appropriate structures, such as investment bonds or family trusts, can provide greater protection and efficiency when transferring wealth. You should consider alternatives to help your clients optimise their estate planning outcomes.

4. Involve children and beneficiaries

Encouraging your clients to involve their children and other beneficiaries in estate planning discussions can boost financial literacy and ensure smoother transitions. Proactively engaging multiple generations helps strengthen relationships, reduce disputes, and increase the retention of FUA for your advice practice.

5. Transfer with certainty

With 74% of estate claims in Australia being successful⁵, it’s critical to help your clients structure their wealth transfers with certainty. Investment bonds, for example, can be held outside the estate, bypassing probate and minimising legal challenges.

6. Stay informed and compliant

You should stay up to date on evolving estate laws and financial regulations to ensure your clients’ estate plans remain valid and effective, without unforeseen legal and tax complications.

7. Manage risks

Identifying risks such as family disputes, potential mismanagement of funds, or legislative changes that could impact wealth transfers, will help you recommend the right structures and prepare your clients accordingly.