Treasurer Jim Chalmers has signalled, before the upcoming Federal Budget in May 2023, the Federal Government’s intention to legislate the purpose of superannuation. The proposed objective will be to “preserve savings to deliver income for a dignified retirement, alongside government support, in an equitable and sustainable way.”ᵃ As part of these changes, the Government will introduce a doubled tax rate on earnings on superannuation balances of more than $3 million, raising the tax rate from 15% to 30%.

There’s now an opportunity for Australians to explore complementary investment options outside of their super.

Investment bonds as a tax effective, complementary option to super

Investment bonds are a stable, tax-effective solution that offer flexibility, control and a range of investment options to suit your lifestyle needs.

Unlike super, investment bond funds are not locked until preservation age or retirement, which means funds can be withdrawn at any time. They are popular with high-income earners seeking to reduce tax, protect assets and want more certainty in estate planning.

Similar to superannuation, investment bonds offer a tax effective solution for building wealth, with tax on investment earnings capped at 30%.

Reduce your tax even further

Generation Life’s proven and market leading tax aware process, takes this one step further and allows us to significantly reduce the impact of tax on investment returns by reducing an investment’s tax assessable earnings by offsetting capital investment losses against income. This can bring the tax rate down to as low as 12-15% over a 15-year period.ᵇ

Through a disciplined tax aware approach to trading when we sell investments such as shares, our process ensures that we effectively manage our clients’ portfolios, selling to deliver the best tax outcome.

For example, the long-term expected increase in after-tax performance of Generation Life’s Tax Optimised series is expected to be between 0.40% and 2.60% p.a.ᶜ when applying these tax aware principles to an investment bond structure. This builds upon the tax arbitrage already available to investors on higher personal marginal tax rates who use the Generation Life investment bond product.

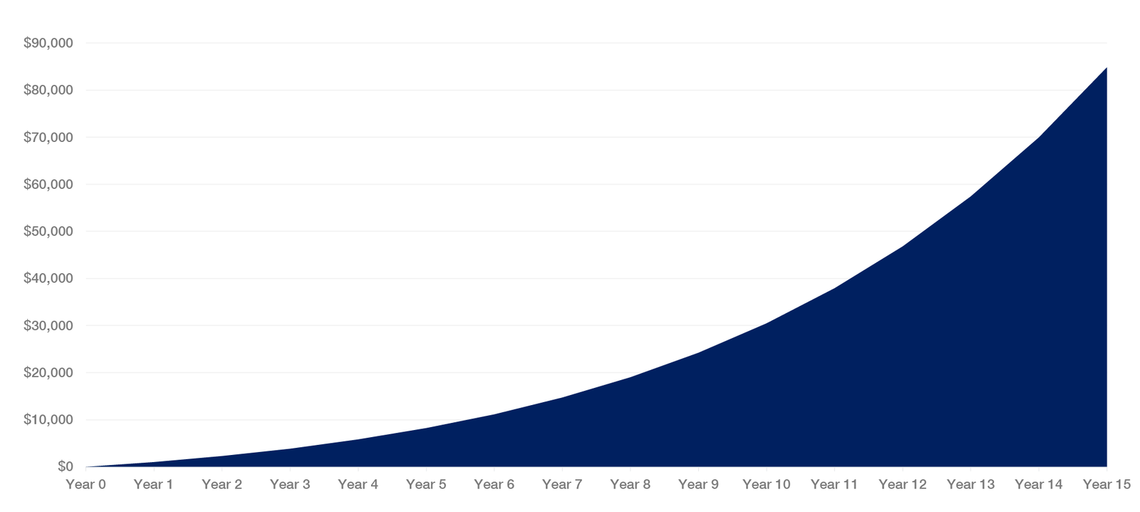

The compounding effect of this process over time can be significant. The longer you are invested, generally the better the after-tax outcome.

Tax is often the largest cost you will incur on your investment—not fees for a financial adviser, platform usage or select products. This is why when it comes to making any investment decision, it’s important to be aware of the impact of tax on your overall investment performance.

After all, investment returns go up when taxes go down. It’s that simple.